Private real estate lending is not a solo venture.

It requires the best team you can find to help you create the best note for you

and your family.

Private lending and your team.

Before we jump into who should be on your team, let’s remember that the cost of each one is normal for borrowers. They’re used to paying for these services. If anyone tries to talk you out of using one or all of these “teammates,” it’s probably a good idea to walk away and find someone else to lend your money to.

Below is the recommended minimum to get a loan properly closed.

Attorney. To make sure your paperwork is legal, proper and protects you.

Closing agent. A third party that handles the paperwork, filings, and money transfers. This is typically an attorney, escrow company, or title company.

Valuation services. A realtor or appraiser who provides an as-is value for the property.

Title company. Provides title insurance to insure you are in the proper lien position (preferably first lien position).

Insurance company. Provides protection from fire or other loss on the property.

You may also wish to hire the following:

Servicing company. Will collect payments and verify taxes and insurance are paid in a timely fashion.

Note company. Help find, underwrite, and close each loan.

Every closing and every state handle private notes/real estate differently, so it’s likely you will have a different team each of you will have a different team.

https://thenoteshop.com/wp-content/uploads/2023/11/21.2.png6281200The Note Shophttps://thenoteshop.com/wp-content/uploads/2020/09/noteshop-logo.pngThe Note Shop2023-11-29 10:53:592023-12-01 11:06:43Private lending and your team

How to lend with your IRA or other retirement plans…private lending with your IRA.

Private real estate notes are a great way to keep your retirement growing nice and steady without the roller coaster ride of the stock market.

But did you know you can fund one of these loans with retirement funds through a company that offers Self Directed IRA Plans?

Most large IRA companies only allow you to invest in stocks and bonds. Self-Directed plans, however, allow you to invest retirement funds in any investment the IRS allows.

This includes real estate and loans.

To invest in private notes using your retirement funds, you must set up an account with a company that offers the Self-Directed options.

Here is a list of some of the companies that offer Self-Directed plans:

The Entrust Group

Equity Trust

Pensco

New Direction IRA

IRA Services Trust Company

Midland Trust

Mainstar Trust

Vantage IRA’s

Of course, you can check the web for other local options, too.

Once you establish an account with one of these companies or another you feel comfortable with, you can start funding loans!

Our suggestion is to select two or three companies you can see yourself working with and shop them for fees and customer service.

Some companies charge just an annual fee, and some charge every time you create or payoff a loan. Other companies might charge you both fees. So, it’s smart to take a few hours and see what best matches your needs.

If you’re interested funding short-term loans (3 to 6-month loans) and have a funds moving back and forth, you might want to stay away from companies that charge larger fees per transaction.

On the other hand, if you’re more interested in long-term loans that go on for years, you probably want to find a cost structure that has a lower annual fee and a larger per transaction fee.

It’s truly up to you and what you’re comfortable with.

So, go check out a couple. Find the fees that match your goals and the customer service reps who will answer the phones and your questions.

If you have any questions on private lending with your IRA you can reach out to us through the contact us form and we would be glad to help.

https://thenoteshop.com/wp-content/uploads/2023/10/FB-Ad-Invest.png6281200The Note Shophttps://thenoteshop.com/wp-content/uploads/2020/09/noteshop-logo.pngThe Note Shop2023-10-27 14:45:562023-10-27 14:53:31Private lending with your IRA

A strong asset and payment stream are the keys to backing all your investments.

How do you do this? By establishing a solid foundation of good returns through good loans.

Good loans are made up of 3 key components:

Good properties

Good borrowers

Good security

Lets start by looking at number 1 in this post and follow up in future posts with 2 and 3.

Good properties.

How can I keep my money working safely for me in any economy?

The first step is to find good loans. And the first step to finding good loans is to find good properties. Because real assets are the BEST way to protect your money.

That’s what I want to chat with you about today.

Good properties.

They are the first foundation block to creating good loans. But what makes a good property?

Here are my top 3 musts:

Must be highly marketable. That means it should be:

In an area of demand

In good condition

A functional home

The property must produce income for the borrower. Think rentals, small commercial or fix and flips (from the sale).

Must be in locations you understand and like. Loan in areas that fit your comfort level. If you are from a small town loan in small towns. If you are from the city put your money to work in the city.

Remember, a real asset (that you like) to protect your investments is the first key building block to good loans.

Ready to build your foundation for good loans? Contact us today and see how we can help you succeed in private lending.

Email us a question at Mike@TheNoteShop.com

Schedule a 30-minute consultation.

Enroll in my personalized coaching services.

Did you enjoy Private notes-Income and Security #1? Check out:

How would you like to lend someone money on a property that you think you’re in a good, secure position with? But then you find out they never owned the property to begin with?

Trust me, it happens.

Everything looks great until payments don’t arrive, and you hire an attorney to foreclose on the property. That’s when you find out the borrower never owned the property and had no right to put a lien on it. Worse, if a lien was actually placed on the property that someone else owns, you will have the extra cost of releasing the lien.

Believe it or not, there are brazen thieves in the world who will fake ownership in properties. They might rent and/or borrow money on them.

So, where does that leave you and your money?

Unfortunately, by the time you discover all of this, most or all of your money will be gone. You’ll probably never find the person who stole it. If you do, they will likely have spent it all.

How do you protect you and your money from a fake owner?

Most thieves are always looking to talk you into a shortcut.

They will tell you, “It’s just a waste of money to involve outside resources for a simple process like a loan.” After all, you both can go right down to the county and record the mortgage or deed (aka, the lien). You can literally watch them hand the lien over to the county and get a receipt to prove it’s recorded.

Guess what?

The county does not check who owns the property when an item is recorded. They simply record what’s handed to them.

So, great. They recorded the lien, but the lien is not valid, and your money is not secured. More likely, it’s gone.

This is another reason you should involve outside resources on such a large money transaction.

The key to stopping thieves is to require every loan be closed, insured, and recorded by a title company. A title company will check and verify the borrower actually owns the property and you’re in the lien position you’re expecting.

If a thief is good and brazen enough to fool the title company, the title company will pay you back your money and write off the loan. But this only happens if you actually pay for a title insurance (aka, a loan title policy).

Title insurance gives you peace of mind that your loan is secured and valid.

Most thieves will never agree to this because they know they’ll get caught. To avoid getting caught, they will try talking you out of purchasing title insurance. They usually do this by pointing out the costs and time involved.

Regarding these so-called costs: If a borrower goes to a traditional lender or bank, they will pay thousands of dollars more than a private lender. So, the cost of title is on the borrower, not you. If they don’t want to pay for title insurance, then fine. They can find another lender and you can find a better borrower; someone who’s grateful and happy to pay a little extra to ensure your funds are secure.

Never listen to a borrower if they claim these costs are nonessential. A quality borrower will be focused on protecting your money by using third party resources, like a title company to close and record.

Private lending Warning #4…OVERFUNDING THE PROPERTY WITH MULTIPLE LOANS

Have you ever had a borrower need money now?

They have the deal of a lifetime and don’t have time to mess with using title for closing. They’ll even record the deed themselves to speed things along. After all, they have successfully closed hundreds of deals, so you can trust them to record your deed.

CODE RED!

DON’T TRUST ANYONE TO CLOSE YOUR DEAL EXCEPT TITLE.

As mentioned above, thieves will try and claim title is just a waste of money and they would rather see you get a better return than throw it away using a title company.

For example, take a look at this $30-million-dollar scam that took place in western Colorado:

A scam artist raised over $30 million from local investors by promising them first deeds of trust on the properties he was buying. To save time and money (or so he claimed) he asked most of the private lenders to come into his office and complete the paperwork. He then took their money and gave them a loan and deed. Each lender thought they were in first lien position.

Unfortunately, they weren’t.

The borrower lied to all of them.

When the Feds finally showed up, all of these lenders were left with about $5 million to split. That might sound like a lot, but it wasn’t. Most of their money and investments had vanished. And it all happened because these lenders chose to trust the borrower and not use a title company to close their loan.

The few who did use title forgot to tell title a very important fact: “I want to be in first lien position.”

So, they too lost most of their money.

Yep, you read that right. If you don’t tell a title company you expect to be in first position, you might end up in a much lower lien position (like 3rd or 4th). That means if something goes wrong with the loan, you’ll have other lenders ahead of you that get paid first.

SO ONLY FUND THROUGH TITLE WITH SPECIFIC INSTRUCTIONS.

Never worry about saving the borrower time and money. Save your time and money from them.

(Check the FBI files to read more about the $30-million scam.)

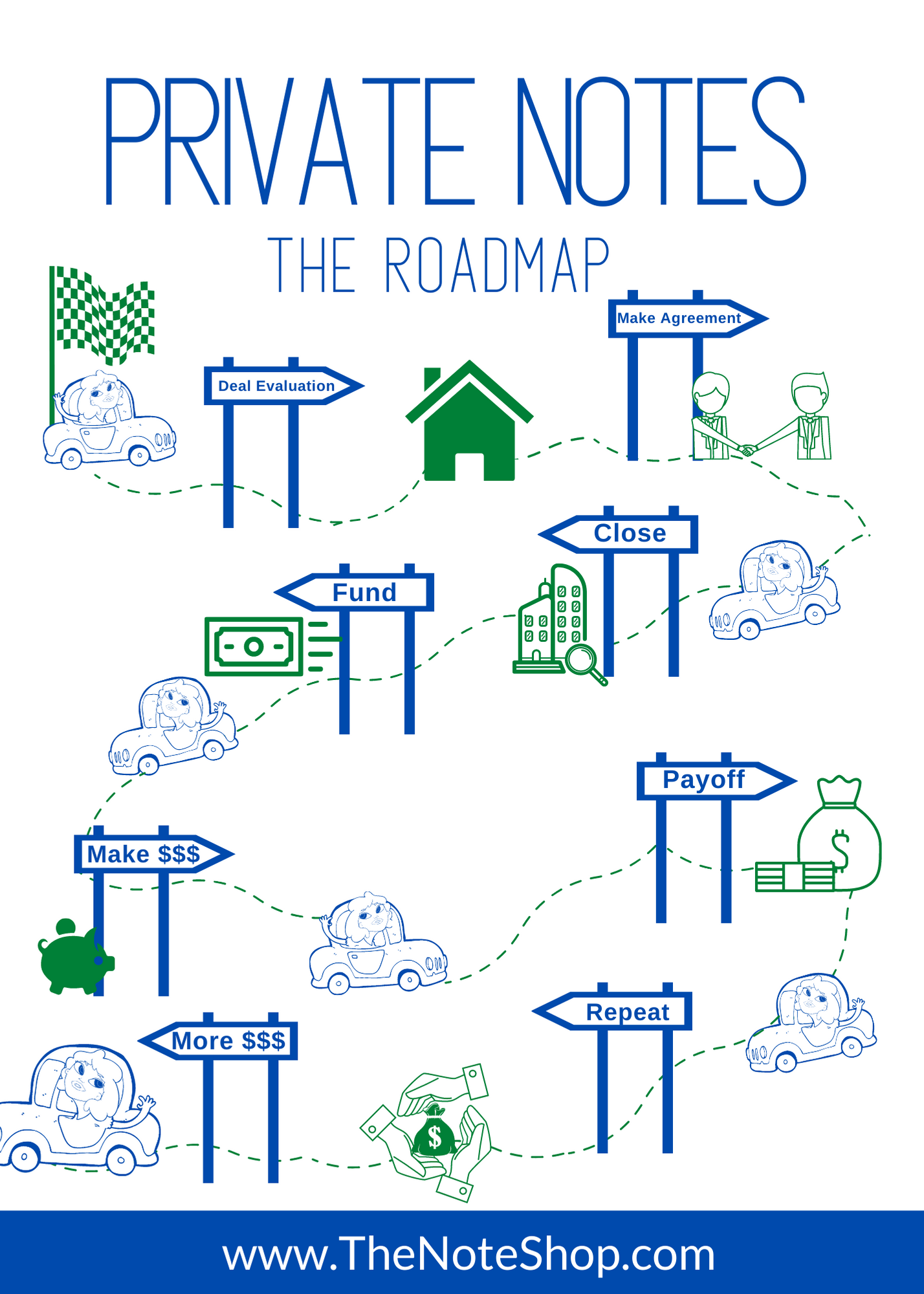

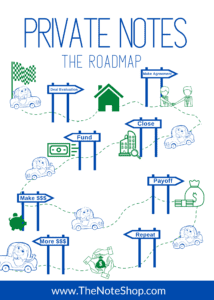

Here is a simple roadmap of the private lending process.

Please use this to just get a overview of how the loan should move through the process.

If you are lending thousands and even hundred of thousands of dollars on notes please take the time to understand the ins and outs of the full note process.

The value of the real estate is your number one protection for your loan. This is the asset behind all the money you’re lending.

It’s the real asset that’ll keep you protected.

But what if that asset isn’t worth as much as the borrower claims?

In all the years I’ve been lending, it still surprises me how far off some people are in their valuation of properties. So many will compare their run-down property to a completely remodeled house and think they would have the same sale price/value. Or they show you a comparable of homes close to their own that are from a higher end subdivision.

For example, my brother lives in a house close to our current office. His home is what I would call a mid-priced home for this area. Within a mile of his home, there are three distinctive subdivisions all separated by a single street. You can tell by driving through the properties they are at different price levels based on the materials used for construction, lot sizes, and amenities.

In this area, the same size house could range from $400k (entry level) to $500k (mid-area), to $750k (nicest subdivision). This is a huge difference in value and what an owner can sell their property for in the future.

Let’s look at an example for a loan of $400k on these properties and evaluate the level of security for the lender (you).

For a home in an entry level subdivision ($400k), your loan will be at the full value of the property. In our opinion, this would be a high-risk investment. What would happen if you had to take the property back and sell it? You would probably lose money with all the costs to foreclose and sell the property. You’d likely walk away from this deal in the red.

For a home in the mid-level subdivision ($500k), you have decent protection with over 30% equity above the loan you have on the property. So, the risk might be worth it.

For the final home in the high-level subdivision ($750k), your security is almost at 50% of the value. So, you’re fairly safe.

Which security would you prefer? Most likely, you’d opt for the higher amount of equity to protect your money.

The problem is, we don’t always know the value of a home. If someone doesn’t know an area very well, they might go online and be blind to the differences between entry, mid, and high-level housing.

It’s also easy for thieves to exaggerate the value and put you in a lien position that doesn’t cover all of your loan.

Exaggerating value is a huge issue.

It shows that the borrower is a thief or that they’re so new to investing, they don’t understand real estate valuation.

How do you protect yourself from over valuation?

If you can, always drive by the house or through the neighborhood to see if there are distinct areas that are different subdivisions.

Hire a professional to value the property for you.

Find an appraiser you can hire or;

Locate a realtor who works in the area and pay them to value the property for you.

Let the experts come up with the value and trust them. They are unbiased and understand the different types of properties and neighborhoods. It’ll be worth your time and peace of mind to spend a few dollars to get professional advice.

Above all else, do not trust the value from the borrower. It doesn’t necessarily mean they are trying to lie to you. They simply might not know the value of the property.

Rely on your own due diligence and that of the professionals you hire to protect your loan.

Private lending Warning #2…NOT USING A THIRD PARTY FOR CLOSING AND DOCUMENTS.

Another popular way for private lenders to get scammed is allowing a borrower to provide all the documents (loan, mortgage, deed etc…).

This might appear to make the process easier for everyone (especially when you don’t have any documents in your back pocket). But it won’t be easier. It’ll only lead to problems. Possibly devastating problems.

Let’s check out an example:

I once had a client, Jennifer, who lent money to a person on one of their homes. This person was a local real estate guru, so Jennifer thought she could trust him. She went ahead and let him write up all of the documents.

He completed them and she funded the deal.

Fast forward six months…

The loan ran into problems and Jennifer wanted to collect.

Guess what she found out? Not only did her borrower not file a lien, but he did little to protect her in the promissory note he created.

When she came to me for help, we discovered the note did not allow for her to collect any attorney fees or default fees. So, the borrower could keep using her money, unless she wanted to pay thousands of dollars out of pocket to collect on the loan.

The best she could do was get her principal back, while he continued to hijack her money at little to no cost.

Why was he able to hijack her money?

Because he wrote up all of the loan documents and MADE IT LEGAL TO STEAL!

I am Michael Bonn, the owner of The Note Shop. For over 23 years, I have been involved in non-traditional and private real estate lending in Colorado and several U.S. states.

My company has been fortunate enough to oversee and close hundreds of millions of dollars in secured real estate notes.

In my experience, I can tell you there’s no better win-win strategy to earn an above market interest rate. Why? Because you’re putting your money to work right in your backyard with local individuals. That means you’re creating jobs where you live.

On top of that, borrowers get easy access to money to keep their portfolio growing, and you’ll find interest rates above those offered by banks, annuities, and bonds. This works great for all funds you are looking to grow without the roller coaster of the stock market. These funds might include:

Savings Accounts

Retirement Accounts

Trust Accounts

Business Accounts

If done correctly, secured private lending on real estate is a great option in all economic environments.

So, with 20 plus years of experience, I have learned what to do and—more importantly—what not to do when lending directly to a borrower.

That’s why I wrote this booklet. It’s intended to show you how to protect yourself and your money by keeping an eye out for scams and other warnings that lead to robbery and headaches.

Of course, there’s no way to list every possible scam or warning in the private lending industry. But these top ten cover the majority of issues you’re most likely to stumble upon during your private lending journey.

Now, be aware, I’m not a lawyer. Therefore, I’d never give or intend to give legal advice. But given the large amount of money you’re looking to lend, I feel it’s vital you understand the possible pitfalls, do your due diligence you, and engage knowledgeable people who can help. That includes a good attorney and title company.

So, without further ado, let’s take a look at

Top 5 WARNINGS

Hijacking a Wire

Why do we see all of these warnings from the local and national title companies and closing agents?

We see these warnings because money is vanishing right before everyone’s eyes. In a flash, hundreds of thousands of dollars are gone!

Every day, money disappears and heads overseas before anyone can do a thing about it. (Yes, the government could control this, but they have chosen not to.) This tragedy happens when both sending money for a new loan and receiving money for a payoff.

What does fraud look like, and how can these thieves grab people’s money and run?

In real estate transactions, the escrow agent, title company, or attorney receive your money and then pay you off later, once the loan is complete. So, money travels back and forth between your account and one of these entities.

During this time, you and an agent will share bank and wire instructions.

This is where a thief likes to get involved.

They’ll find a way to hack into a communication system and add information that looks like it’s coming from someone involved, be it the closing agent, realtor, borrower, etc. Their goal is to convince you that the wire instructions changed.

With this change, the thief asks you to wire the funds to a different account. They usually also ask you to wire funds sooner than agreed upon. Why? Because they need the extra time to make sure the money is moved through the banking system before closing…and before you can get it back.

All of this might happen to you via email, text, or a phone call.

Thieves are tricky. They will find a way to break into a stream of email or text communication and make it look like the communication is coming from the same source.

What can you do?

Get on the phone and verify wire instructions.

It doesn’t matter if the instructions were sent through a super high-level security system (ex: encrypted email). A hacker can find a way around those. You shouldn’t even trust the phone numbers listed on a closing agent’s email. Take a few minutes to go online and look your agent’s phone number up. Make sure they match.

It all comes down to doing your due diligence. With every wire, call and verbally verify with the correctagent the instructions you’re supposed to use. Walk through each item and verify:

Bank name

Account name

Account number

ABA or routing number

The agent’s file name or number

NEVER accept last minute changes to wire instructions.

ALWAYS verify instructions before you send or receive a wire.

When you receive a wire, demand that the person sending you money verbally verifies the information with you and only you.

This alone can save you and your life savings.

Let’s take a look at some real-life examples.

Note: Do not solely rely on these examples as the only way thieves will try to steal your money. Although I’ll attempt to give you as many examples as possible throughout this booklet, I cannot possibly know them all. So, always get to know who is handling your transactions and ask them the best practices to keep your money safe.

The following happened to two lenders I know personally. One of them lost a couple hundred thousand dollars, and the other saved his funds at the last minute.

Let’s call the first lender Bob.

Bob had an arrangement with his bank to simply wire funds when they received a fax from him. Somehow a thief broke into Bob’s system and found his form for faxing wire requests. The thief created their own request and had funds wired to them out of the country before Bob could find out.

The bank was not responsible. Bob was.

So, he lost it all.

Now, let’s call the second lender Joe.

Joe had someone hack into his email, clone a message, and change the wire instructions. What do I mean by “cloning”? Well, let’s say Joe’s email was Joe@TheNoteShop.com. The thief went in and created a similar email address that most people would not notice, like Joe@TheNoteShops.com. By adding one letter (s) at the end of the address, the thief changed the email. Again, most people would not notice the change and thieves can quietly sneak by.

That’s what happened to Joe. Someone changed the wire instructions by creating a similar email address. The wire was readied to go out, but—thankfully—someone noticed the name on the account looked wrong. So, they did a verbal verification as a safety precaution.

Joe’s money was saved.

Here’s another example I recently read about:

A property in Colorado did not close because the money to purchase was diverted by a text message. The person received a text that they thought came from the realtor involved in the transaction. The text asked them to wire their funds a day early to a new account. On the day of closing, they realized they’d been scammed, and the money was gone.

So, as you can see, there many reasons why emails from closing agents warn of wire fraud.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.